Venture trends we'll see in the next decade

Predictions: acquisitions galore, more capital pouring into late-stage secondaries. Also this week: OpenAI shifts away from Nvidia chips, and will we see Apple x Perplexity?

The funding landscape has been shifting dramatically post-ZIRP. I’ve compiled some observations, and built in a few predictions on how venture will change over the next decade. In the most radical of my projections, I would say that the majority of VC funds today will be irrelevant in its current form in the next 10 years.

We will see a lot more consolidation in the later rounds, and likely a lot more fragmentation in the early-stages. We will see retail-oriented platforms dominating in late-stage secondaries or pre-IPO trades. We will see more private equity and real estate plays (not just from VC firms) to capitalize on this technology wave.

These predictions are grounded in some data, but still speculative in nature!

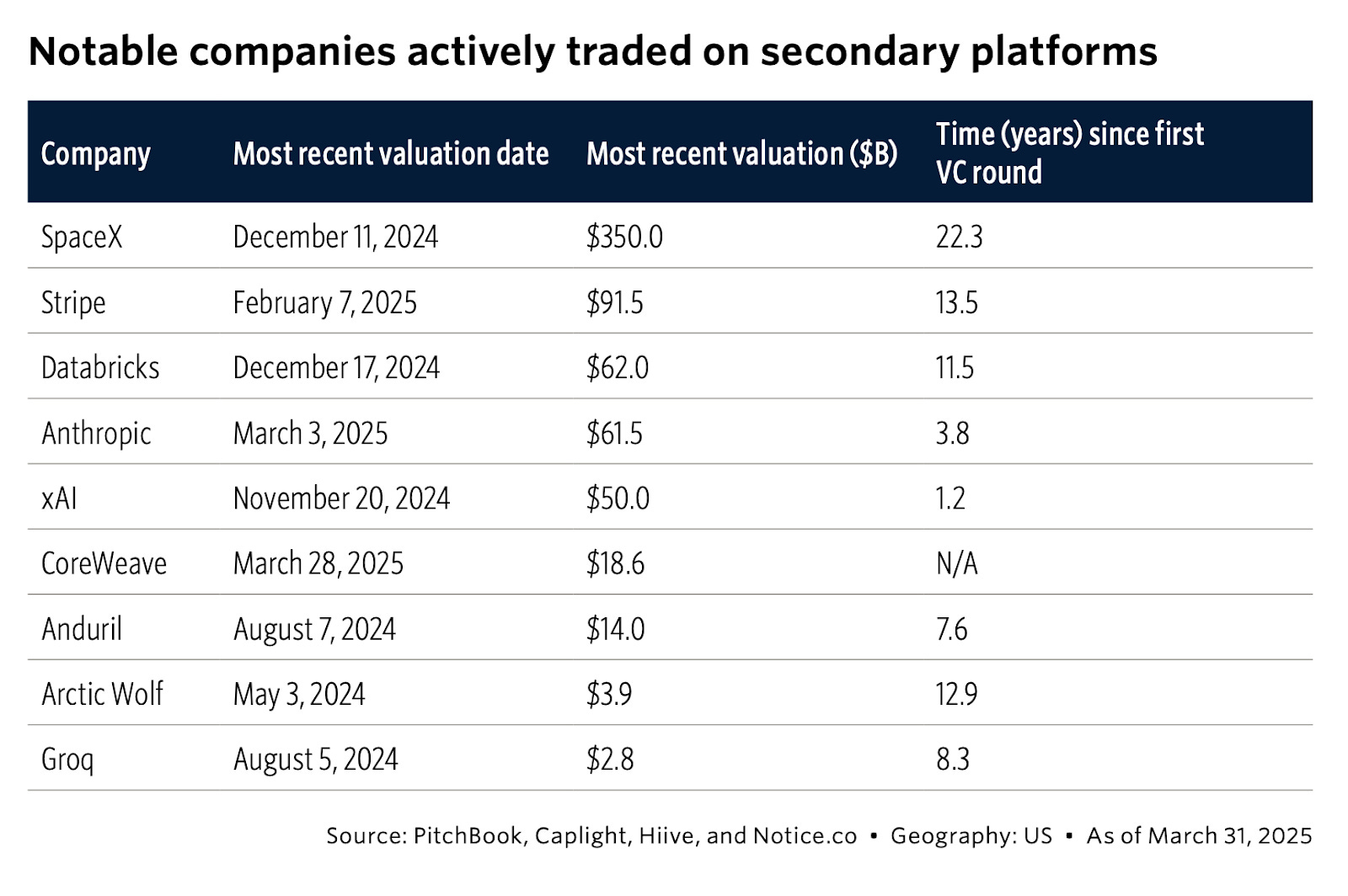

1. Late-stage private markets will pull in even more capital.

In the last few years, US liquidity channels have flipped from IPOs to secondaries. As a data point: from 2019 to 2021, US IPO proceeds were about 2 to 4x larger than VC secondaries. By 2024, VC direct secondaries (think, GP-led deals or employee tenders) are now almost double that of the US IPO proceeds, and growing 20% year-on-year.

Whether or not the IPO windows ease up over the next few years, there are clear signs that there is heavy interest and demand from new capital to access the private markets. There’s a heavy emphasis on brand - similar to how “The Magnificent Seven” drives a significant portion of the S&P 500’s performance, secondary transactions are concentrated among a small group of top-tier startups.

Consolidation seems inevitable in this asset class. Capital, especially retail, will likely gravitate towards a handful of well-known venture brands or platforms (e.g. Forge, Hiive, Caplight) that can successfully market to retail investors and private capital.

2. Anchors and Titans will aggressively acquire

Young startups with early distribution, technical brilliance, or viral UX hooks will continue to be acquired quickly, sometimes within months. Others will get copied. The Titans and Anchor archetypes will use balance-sheet cash to snap up promising startups with any sign of distribution, data, or AI talent.

This quarter alone (Q1 2025), there were 550 M&A deals involving venture-backed startups, totaling about $71 billion in exit value - the highest dollar volume since 2021. Most of the high-profile deals were in AI , with 81 AI-related M&A like Wiz ($32B), Ampere Computing ($6.5B), Weights & Biases (~$1.7B).

This pace has continued well into Q2 2025, with acquisitions like Codeium ($3B), Scale ($14.3B), Jony Ive’s I/O ($6B).

PE firms are moving in as well, and ramping up their startup purchases. Crunchbase reports that private equity firms spent more than $56 billion in disclosed-price deals (the real number is likely 5x more).

3. There will be more Lean Giants

Many of them will sell picks and shovels into the AI boom, i.e. serving builders rather than end-users. These may be software plays, or service providers or infrastructure.

We will see lean teams pull outsized revenues per employee. For instance, CoreWeave’s ~$3.5 M revenue per employee is about 30× the median private-SaaS benchmark.

New companies that can move quickly to capitalize on supply-side pull (GPU demand, energy-efficient compute, data-labeling for training) will create multi-billion-dollar niches where small, execution-heavy teams can thrive.

Becoming part of the AI infrastructure flywheel is key for these Lean Giants, as adoption across the ecosystem will make it easier for them to capture value (and a moat) over time, without directly chasing end-user markets.

I also see private equity playing a heavier role here, who aren’t as reticent as venture to lean into services-driven sales. We’re seeing some emergent “venture roll-ups” like acquiring accounting firms and enhance their profit margin with AI. Maybe we’ll see more partnerships between private equity and real estate infrastructure players with VC or tech insiders.

4. New types of financing to serve the Super Solos

The solo SaaS startups (Super Solos making $1 - $5M ARR) isn’t a fit for traditional venture returns, who are looking for billion-dollar breakouts. The truth is, most AI startups today aren’t venture-like, and shouldn’t be overcapitalized to be.

There’s an opportunity for a new breed of funds or financing structures to serve this emerging startup archetype - blending early-stage bets with revenue-share financing. Returns might be capped (say, at 3 - 5x returns), but cash distributions can happen as the company grows. Most revenue-based financing or private credit products start at $200K min ARR - with the rise of solo SaaS, there could be appetite to take earlier bets like in venture, with better economics than RBF.

Just as a back-of-napkin thought exercise:

Fund size: $50 M, deployed as 500 x $100 k revenue-share checks.

Terms: 5× cap on each check; monthly rev-share until cap is hit.

Outcomes (assuming 60 % hit the cap in 4 years, 20 % return 2× in 4 years, 20 % fail):

Gross MOIC: 3.4x

Gross IRR (4 years): ~36%

As a comparison, traditional VC could get to 3.4x, but in about 10 years. This is more of a thought exercise, but I’m curious if a capped-return, revenue-share fund can land venture-like multiples with materially faster paybacks, appealing to LPs who are looking for shorter-cycle vehicles and quicker liquidity.

Note from reader Madhu Chamathy:

One suggested addition: revenue-based financing for AI infra plays. The most powerful proof of this shift is CoreWeave's $7.5 billion debt financing, which I believe is one of the largest debt financings ever. Out of their $12 billion, $8 billion is in debt at ~14% interest. Lambda also did $500MM debt financing.

In a way, such AI infra companies are more like utilities vs. software companies (assuming they have predictable revenue, for e.g. from hyperscalers). This kind of capital play is very different from the venture playbook.

5. More private capital into moonshot bets

We are seeing an increasingly informed flow of private capital into moonshot bets that benefit humanity. Like the AI scientist non-profit Future House to Astera (a non-profit foundation focused on life sciences and space), dollars are channeling into big bets that could define the next era of humanity.

This capital is patient and thesis-driven, and might be a much-needed, dynamic complement to federal or academic funding.

It will be more important than ever for investors (GPs and LPs) to stay agile over the next decade. The venture playbook has never been stagnant throughout the decades, and the upcoming cycle will be more transformative than ever. It takes experimentation, boldness, and grounding to capitalize on shifting sands.

Have a great weekend - ttyl

The Download —

News that mattered this week

Google convinces OpenAI to use their TPU Chips instead of Nvidia’s. This is the first time it has used non-Nvidia chips in a meaningful way, according to a person who is involved in the arrangement. The move reflects OpenAI’s broader shift away from relying on Microsoft data centers and could boost Google’s tensor processing units as a cheaper alternative.

OpenAI might be stealth-building the ultimate Google Workspace and Office 365 replacement: The new features reportedly include collaborative document editing capabilities, like those offered by Google Docs, along with meeting transcription and a team chat function.

Anthropic now lets you make apps right from its Claude AI chatbot: Anthropic is adding a new feature to its Claude AI chatbot that lets you build AI-powered apps right inside the app. It basically sounds like vibe coding, but with the ability to see the results right inside Claude.

Google rolls out new Gemini model that can run on robots locally: Google DeepMind released a new language model called Gemini Robotics On-Device that can run tasks locally on robots without requiring an internet connection.

OpenAI and io fae lawsuit over branding conflict: OpenAI and hardware startup io, founded by former Apple designer Jony Ive, are now embroiled in a trademark infringement lawsuit filed by Iyo, a Google-backed company specialising in custom headphones. Iyo has sued the pair for allegedly stealing its product concepts and trademarked name.

MIT’s new SEAL framework lets models teach themselves: Researchers at MIT have developed a framework called Self-Adapting Language Models (SEAL) that enables LLMs to continuously learn and adapt by updating their own internal parameters. SEAL teaches an LLM to generate its own training data and update instructions, allowing it to permanently absorb new knowledge and learn new tasks.

Mira Murati’s Thinking Machines Lab closes on $2B at $10B valuation: Thinking Machines Lab, the secretive AI startup founded by OpenAI’s former chief technology officer Mira Murati, has closed a $2 billion seed round, according to The Financial Times. The deal values the 6-month-old startup at $10 billion.

DeepMind launches AlphaGenome to predict how DNA mutations affect genes: Google DeepMind introduced AlphaGenome, a new AI tool that can comprehensively predict how mutations or variants in human DNA sequences impact gene regulation. The genome is the complete set of deoxyribonucleic acid, or DNA, within a living cell, which includes all the genetic information necessary for development, growth and functioning.

Apple is reportedly considering buying Perplexity AI in its biggest-ever acquisition: According to a new Bloomberg report, Apple's head of mergers and acquisitions, Adrian Perica, has been in talks with services SVP Eddy Cue and the company's top executives about a potential offer. Another possibility is a team-up with Perplexity, rather than an acquisition.

Databricks & Perplexity co-founder Andy Konwinski launched the Laude Institute with $100M. The non-profit will convene, resource, and amplify computer scientists to help them fast-track breakthroughs for real-world impact.

Double Click —

Links to reads we found interesting

AI agents will threaten humans to achieve their goals, Anthropic report finds (ZDNet)

Vera Rubin Space Telescope releases first images from its 3,200 megapixel camera (Yahoo News)

Scientists working to decode signal from earliest years of universe (Futurism)

New study claims AI 'understands' emotion better than us – especially in emotionally charged situations (Live Science)