The Shifting Sands of Venture Post-ZIRP

The funding landscape has been shifting dramatically post-ZIRP. In the most radical projections, I would say that the majority of VC funds today will be irrelevant in its current form.

Scale AI’s biggest competitor is a company most people have never heard of.

It brought in $1B in revenue last year, surpassing Scale’s $850M.

Entirely bootstrapped. Not a single dollar of VC funding raised.

We talk a ton about how AI is changing how software is written. I think this technology cycle will fundamentally change how companies are funded.

As a caveat, this is not just because of AI, but it is, of course, part of the catalytic forces.

First, a rising taxonomy with new company Archetypes I’ve observed in the past few years:

┌────────TITANS (ARR $150-400B)────────┐

│ Alphabet · Apple · Microsoft · │

│ Meta · Nvidia (ARR $150-400B) │

└──────────────────────────────────────┘

─────── ANCHORS (ARR $3-10B) ───────

OpenAI · Anthropic · Snowflake · Databricks

─────── LEAN GIANTS (ARR $500M-1B) ───────

Cursor · Surge

─────── FAST CLIMBERS (ARR $20-100M) ───────

Supabase · Vercel · Genspark · Gamma ·

Lovable · Harvey · Glean

─────── SUPER SOLOS (ARR $1-5M) ───────

Base44 The Super Solos ($1 - 5M ARR)

Solo founders or ultra-lean teams building with agentic tools like Cursor or Lovable. Typically bootstrapped or lightly funded. Products show early breakout traction and are often acquired within 6 to 12 months for talent, distribution, or product love.

Looks like:

Base44, a prompt-to-code app acquired by Wix for $80M this week. It was generating $3.5M ARR, and reportedly grew to 250,000 users in 6 months. At this stage, the Solo startups tend to be high-growth, low-profitability: Base44 netted out at $189,000 in profit in May on its $3.5M ARR, after covering high LLM token costs.

The Fast-Climbers ($20M - $100M ARR)

Startups that have quickly captured the imagination and attention of the early adopters. Many developers consider them as core to the new software stack. Tends to be highly collaborative within the ecosystem. Fast-growing, but early revenue may not be an indication of long-term user retention as early-adopters can be flaky in loyalty.

Looks like:

Supabase ($20M ARR), Vercel ($20M ARR), Genspark ($36M ARR), Gamma ($50M ARR), Lovable ($75M ARR), Harvey ($75M ARR), Glean ($100M ARR)

*numbers are estimates from what I could find online.

** There are a few in-betweeners like Hugging Face ($130M ARR) and Windsurf ($100M ARR) who could be on their way up to the next tier.

The Lean Giants ($500M - $1B ARR)

Companies operating at scale with surprisingly small teams. Some are heavily venture-funded; others, like Surge, are entirely bootstrapped. They’ve locked in real enterprise traction and are not slowing down any time soon. Typically lean teams, with remarkably high revenue per employee.

Looks like:

Cursor ($500M ARR; ~50 person team; raised >$1B VC funding)

Surge ($1B ARR; ~100 person team; raised $0 VC funding)

The Anchors ($3 - $10B ARR)

These are the foundational players driving the AI cycle. They’re building the infrastructure like models, platforms, protocols, and products that others build on.

Looks like:

OpenAI ($10B ARR), Anthropic ($3B ARR), Snowflake ($3.8B ARR), Databricks ($2.8B ARR)

The Titans ($150B - $350B ARR)

Tech giants dominating capital, distribution, and compute. They’re integrating AI into everything, from chips to cloud to consumer.

Looks like:

Alphabet ($350B ARR), Apple ($400B ARR), Microsoft ($245B ARR), Meta ($170B ARR), Nvidia ($150B ARR)

So where does venture go from here?

The funding landscape has been shifting dramatically post-ZIRP. I’ve compiled some observations, and built in a few predictions on how venture will change over the next decade. In the most radical of my projections, I would say that the majority of VC funds today will be irrelevant in its current form in the next 10 years.

We will see a lot more consolidation in the later rounds, and likely a lot more fragmentation in the early-stages. We will see retail-oriented platforms dominating in late-stage secondaries or pre-IPO trades. We will see more private equity and real estate plays (not just from VC firms) to capitalize on this technology wave.

These predictions are grounded in some data, but still speculative in nature!

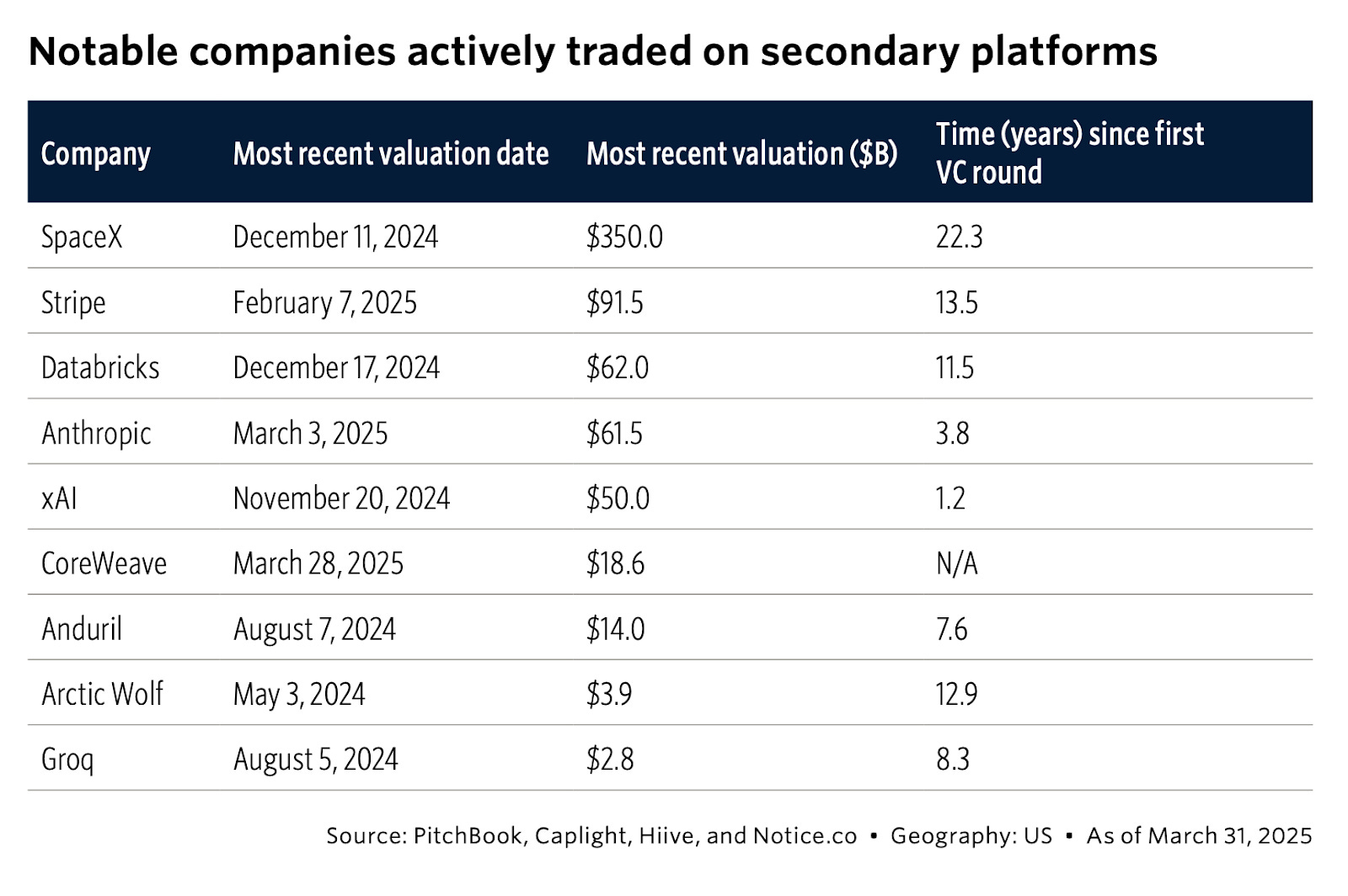

1. Late-stage private markets will pull in even more capital.

In the last few years, US liquidity channels have flipped from IPOs to secondaries. As a data point: from 2019 to 2021, US IPO proceeds were about 2 to 4x larger than VC secondaries. By 2024, VC direct secondaries (think, GP-led deals or employee tenders) are now almost double that of the US IPO proceeds, and growing 20% year-on-year.

Whether or not the IPO windows ease up over the next few years, there are clear signs that there is heavy interest and demand from new capital to access the private markets. There’s a heavy emphasis on brand - similar to how “The Magnificent Seven” drives a significant portion of the S&P 500’s performance, secondary transactions are concentrated among a small group of top-tier startups.

Consolidation seems inevitable in this asset class. Capital, especially retail, will likely gravitate towards a handful of well-known venture brands or platforms (e.g. Forge, Hiive, Caplight) that can successfully market to retail investors and private capital.

2. Anchors and Titans will aggressively acquire

Young startups with early distribution, technical brilliance, or viral UX hooks will continue to be acquired quickly, sometimes within months. Others will get copied. The Titans and Anchor archetypes will use balance-sheet cash to snap up promising startups with any sign of distribution, data, or AI talent.

This quarter alone (Q1 2025), there were 550 M&A deals involving venture-backed startups, totaling about $71 billion in exit value - the highest dollar volume since 2021. Most of the high-profile deals were in AI , with 81 AI-related M&A like Wiz ($32B), Ampere Computing ($6.5B), Weights & Biases (~$1.7B).

This pace has continued well into Q2 2025, with acquisitions like Codeium ($3B), Scale ($14.3B), Jony Ive’s I/O ($6B).

PE firms are moving in as well, and ramping up their startup purchases. Crunchbase reports that private equity firms spent more than $56 billion in disclosed-price deals (the real number is likely 5x more).

3. There will be more Lean Giants

Many of them will sell picks and shovels into the AI boom, i.e. serving builders rather than end-users. These may be software plays, or service providers or infrastructure.

We will see lean teams pull outsized revenues per employee. For instance, CoreWeave’s ~$3.5 M revenue per employee is about 30× the median private-SaaS benchmark.

New companies that can move quickly to capitalize on supply-side pull (GPU demand, energy-efficient compute, data-labeling for training) will create multi-billion-dollar niches where small, execution-heavy teams can thrive.

Becoming part of the AI infrastructure flywheel is key for these Lean Giants, as adoption across the ecosystem will make it easier for them to capture value (and a moat) over time, without directly chasing end-user markets.

I also see private equity playing a heavier role here, who aren’t as reticent as venture to lean into services-driven sales. We’re seeing some emergent “venture roll-ups” like acquiring accounting firms and enhance their profit margin with AI. Maybe we’ll see more partnerships between private equity and real estate infrastructure players with VC or tech insiders.

4. New types of financing to serve the Super Solos

The solo SaaS startups (Super Solos making $1 - $5M ARR) isn’t a fit for traditional venture returns, who are looking for billion-dollar breakouts. The truth is, most AI startups today aren’t venture-like, and shouldn’t be overcapitalized to be.

There’s an opportunity for a new breed of funds or financing structures to serve this emerging startup archetype - blending early-stage bets with revenue-share financing. Returns might be capped (say, at 3 - 5x returns), but cash distributions can happen as the company grows. Most revenue-based financing or private credit products start at $200K min ARR - with the rise of solo SaaS, there could be appetite to take earlier bets like in venture, with better economics than RBF.

Just as a back-of-napkin thought exercise:

Fund size: $50 M, deployed as 500 x $100 k revenue-share checks.

Terms: 5× cap on each check; monthly rev-share until cap is hit.

Outcomes (assuming 60 % hit the cap in 4 years, 20 % return 2× in 4 years, 20 % fail):

Gross MOIC: 3.4x

Gross IRR (4 years): ~36%

As a comparison, traditional VC could get to 3.4x, but in about 10 years. This is more of a thought exercise, but I’m curious if a capped-return, revenue-share fund can land venture-like multiples with materially faster paybacks, appealing to LPs who are looking for shorter-cycle vehicles and quicker liquidity.

Note from reader Madhu Chamathy:

One suggested addition: revenue-based financing for AI infra plays. The most powerful proof of this shift is CoreWeave's $7.5 billion debt financing, which I believe is one of the largest debt financings ever. Out of their $12 billion, $8 billion is in debt at ~14% interest. Lambda also did $500MM debt financing.

In a way, such AI infra companies are more like utilities vs. software companies (assuming they have predictable revenue, for e.g. from hyperscalers). This kind of capital play is very different from the venture playbook.

5. More private capital into moonshot bets

We are seeing an increasingly informed flow of private capital into moonshot bets that benefit humanity. Like the AI scientist non-profit Future House to Astera (a non-profit foundation focused on life sciences and space), dollars are channeling into big bets that could define the next era of humanity.

This capital is patient and thesis-driven, and might be a much-needed, dynamic complement to federal or academic funding.

Conclusion

It will be more important than ever for investors (GPs and LPs) to stay agile over the next decade. The venture playbook has never been stagnant throughout the decades, and the upcoming cycle will be more transformative than ever. It takes experimentation, boldness, and grounding to capitalize on shifting sands.

If you enjoyed this piece, please share it! and follow our work at Strange Ventures, a first-check firm investing in the future of computing.